Introduction

Active-Duty Military Families often balance mobility, duty station changes, family size, and real housing needs, so it makes sense to want homebuying tips that feel simple, supportive, and clear.

VA Loan benefits can make the process easier with eligibility options, 0% down payment, no PMI, and a more confident starting point. PCS (Permanent Change of Station) timing can add uncertainty, but the right plan helps you think through relocation, assignment changes, hold period, and the buy-vs-rent decision with less stress.

BAH (Basic Allowance for Housing) can give your budget a smart foundation by helping you match your monthly allowance to a home that feels comfortable and sustainable. Property decisions get easier when you focus on proximity to base, price, condition, resale potential, and rental potential, and this guide will help you move forward with clarity and confidence.

Can You Buy a Home While on Active Duty?

Many service members wonder if buying a home is feasible while actively serving. The answer is yes, but timing and planning are key.

Active-duty members often face unique challenges, including frequent relocations (PCS) and potential deployments. These factors can affect both the choice of home and financial strategy.

Eligibility Criteria

To buy a home on active duty, you must meet service requirements, which vary slightly depending on branch and length of service. Most active-duty members are eligible for VA loans, which reduce the financial burden of purchasing a home.

Key Benefits

- VA Loans with lower interest rates and minimal down payments make it easier to buy a home

- SCRA Protections provide safeguards during active duty, including protection from foreclosure

Understanding VA Loans and Benefits

One of the most significant advantages of buying a home as an active-duty service member is access to VA loans. These loans are designed to support military families with favorable terms that are not available through conventional mortgages.

What Is a VA Loan?

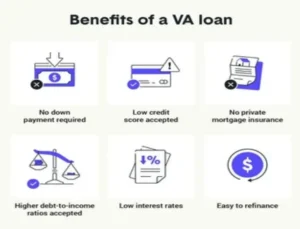

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs. Unlike traditional loans, VA loans often require no down payment and do not require private mortgage insurance (PMI). Interest rates are usually lower, making it more affordable for military families.

Benefits Compared to Conventional Loans

- No down payment required

- No PMI

- Lower interest rates

- Flexible qualification criteria

How to Get a Certificate of Eligibility (COE)

Before applying, you need a COE, which verifies your military service. You can obtain it online through the VA portal, through your lender, or at your regional VA office.

Avoiding Common Pitfalls

- Funding Fee may apply, but it can be waived for those with service-connected disabilities

- Loan Limits should be checked to ensure you remain eligible for maximum benefits

How to Prepare Financially Before Buying

Even with VA loan benefits, financial preparation is critical for a successful home purchase.

Improve Credit Score

A solid credit score helps secure better loan terms. While VA loans are flexible, a score above 620 is ideal.

Budgeting

Even with no down payment, plan for:

- Closing costs

- Home inspections

- BAH (Basic Allowance for Housing) coverage to ensure mortgage affordability

PCS-Related Planning

Frequent relocations are part of military life. Before buying, consider whether you may need to sell quickly or rent out your home. Planning ahead reduces financial stress and ensures smoother transitions.

Finding the Right Home and Location

Choosing the right home and location is just as important as financing.

- Proximity to Base Homes near military installations often hold value and reduce commute stress

- Rental Income Options Renting your home can cover mortgage payments if a PCS move is coming

- Military-Savvy Real Estate Agents Agents familiar with VA loans and military relocations can streamline the process and prevent costly mistakes

The Homebuying Process for Active Duty Families

The homebuying process is similar to civilian buyers but there are unique considerations for active-duty families.

- Pre-Approval Get VA loan pre-approval to set your budget and demonstrate seriousness to sellers

- House Hunting Focus on homes that meet your family’s needs and are near your duty station

- Making an Offer Work with your agent to make competitive offers while keeping PCS timelines in mind

- Inspection and Appraisal VA loans require appraisals to ensure the property meets minimum property standards; independent inspections are also recommended

- Closing Coordinate dates carefully, especially if deployment or PCS is imminent. Some lenders offer remote closings for military members

Common Mistakes Military Families Make

Even experienced service members can encounter challenges when buying a home. Avoid these common mistakes:

- Ignoring PCS or deployment, which can lead to financial strain

- Overlooking VA loan benefits, which can cost thousands in interest and fees

- Overestimating BAH coverage, which may not fully cover mortgage costs in high-cost areas

- Skipping neighborhood research, including safety, commute, and schools

Conclusion

Buying a home while on active duty is entirely possible, but it requires preparation, knowledge of VA loan benefits, and strategic planning. Military families who plan financially, leverage their VA benefits, and work with knowledgeable professionals are more likely to have a smooth homebuying experience.