Introduction to Military Mortgage Calculators

Buying a home while serving in the military can feel like trying to hit a moving target. Between deployments, frequent relocations, and the complexities of VA loan benefits, figuring out what you can truly afford isn’t simple. That’s why a military mortgage calculator is more than just another online tool. It’s a critical resource designed for service members who want clarity and confidence in their homebuying decisions.

Why Service Members Need Specialized Mortgage Tools

Traditional mortgage calculators don’t account for the unique aspects of military pay and benefits. Service members often receive non-taxable income like the Basic Allowance for Housing (BAH), which significantly affects how much home they can afford. They may also qualify for VA loans, which remove the need for a down payment and private mortgage insurance.

Without a calculator that factors in these elements, the numbers can be misleading. A military mortgage calculator brings everything together: your pay, your benefits, and your potential loan terms to give you a more accurate financial picture.

Key Differences Between Civilian and Military Mortgage Calculators

A regular mortgage calculator only looks at your gross income, interest rate, and loan term. A military calculator, on the other hand, integrates:

- BAH (Basic Allowance for Housing)

- VA loan limits and funding fees

- Tax-exempt income portions

- PCS (Permanent Change of Station) considerations

These differences matter. For example, a civilian earning $60,000 might afford less than a service member earning the same base pay plus BAH, because that allowance boosts total available income without increasing taxable income.

How the Military Mortgage Calculator Works

Inputting Loan Amount, Interest Rate, and Term

Like any calculator, you’ll start by entering the loan amount, interest rate, and term (usually 15 or 30 years). The tool then estimates your monthly principal and interest payment.

For accuracy, make sure your interest rate reflects current VA loan rates, which are often lower than conventional loans due to federal backing.

Factoring in Basic Allowance for Housing (BAH)

BAH is a game-changer for military borrowers. It’s designed to offset housing costs and varies by rank, duty station, and whether you have dependents. When you include your BAH in the calculator, it helps determine how much of your income can comfortably go toward a mortgage payment.

A smart approach is to treat your BAH as your housing budget ceiling, not your target. That way, you build in financial breathing room for other expenses.

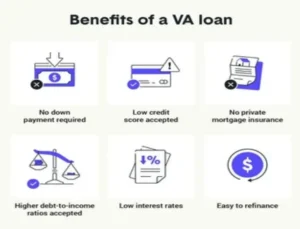

Understanding VA Loan Funding Fees and How They Impact Payments

VA loans come with a funding fee, a one-time charge that supports the program and replaces the need for monthly mortgage insurance. The fee depends on your down payment (if any) and whether it’s your first or subsequent VA loan.

You can either pay it upfront or roll it into your mortgage. The calculator can show you how including it in the loan balance affects your monthly payment and total interest over time.

Estimating Home Affordability for Service Members

How to Calculate Monthly Mortgage Payments

Once the calculator processes your inputs, it estimates your monthly payment, including principal, interest, taxes, and insurance (PITI). To get a realistic number, make sure you include local property tax rates and homeowner’s insurance estimates.

Determining How Much House You Can Afford on Military Pay

A good rule of thumb: your total housing costs shouldn’t exceed 28–30% of your gross monthly income, including BAH. But because BAH isn’t taxed, your effective income is higher than it looks on paper, so you might qualify for more than you think.

Still, lenders consider your debt-to-income ratio (DTI) when approving loans. Keeping your DTI below 41% (including your new mortgage payment) makes approval more likely and ensures you’re not overextending.

Accounting for Taxes, Insurance, and HOA Fees

Even with a VA loan, there are costs beyond the mortgage payment. Property taxes vary widely by state and county, and HOA fees can add hundreds to your monthly expenses. A comprehensive military mortgage calculator includes these to prevent unpleasant surprises after closing.

Using VA Loan Benefits with the Calculator

No Down Payment Advantage for VA Loans

One of the biggest perks of a VA loan is no required down payment for most borrowers. That can free up your savings for closing costs, home improvements, or emergencies. Use the calculator to compare how different down payment amounts (0%, 5%, or 10%) affect your monthly payment and total loan cost.

Comparing VA Loans to Conventional and FHA Options

It’s worth using the calculator to compare loan types side by side. Conventional loans may have stricter credit requirements and require mortgage insurance unless you put down at least 20%. FHA loans require at least 3.5% down plus monthly insurance premiums. A VA loan often comes out ahead, especially if you’re eligible and plan to stay in the home long enough to offset the funding fee.

How VA Loan Limits Affect Home Affordability

While the VA doesn’t cap how much you can borrow, it does limit the amount it guarantees for lenders. In most cases, this isn’t a problem, but in high-cost areas, you might need a small down payment if your loan exceeds the local limit. The calculator helps you see exactly how that affects your affordability range.

Budgeting and Planning for Homeownership

Tips for Saving for Homeownership on Military Pay

Even without a down payment, you’ll still need money for closing costs, maintenance, and emergencies. Start small by setting aside a portion of your BAH each month. Automating these savings can make it painless and consistent.

Some service members also use Thrift Savings Plan (TSP) funds for housing-related expenses, but that should be done carefully to avoid long-term retirement impacts.

Creating a Realistic Budget for Home Expenses

A house payment is just one piece of the puzzle. Budget for utilities, maintenance, and repairs, which can easily total 1-2% of your home’s value each year. A realistic budget prevents financial strain, especially if you’re deployed or relocate frequently.

Avoiding Common Mistakes When Estimating Affordability

A few pitfalls to avoid:

- Ignoring PCS-related expenses

- Underestimating taxes or insurance

- Assuming BAH won’t change (it can, depending on duty station)

- Forgetting about closing costs or furniture purchases

Being conservative with your estimates is better than stretching too thin.

Tools and Resources for Smarter Military Home Buying

Online Mortgage Calculators for Service Members

Several reputable sites offer free military mortgage and affordability calculators.

Housing Assistance Programs That Complement VA Loans

Programs like HomeStrong USA, Operation Homefront, and state-based first-time homebuyer assistance programs can help with down payments or closing costs. Combining these with VA benefits can make homeownership more attainable.

Working with Military-Friendly Lenders and Advisors

Choose lenders who specialize in VA loans and understand the nuances of military life. They can guide you through the process, ensure your paperwork is correct, and help you get the best rate for your situation.

Conclusion and Next Steps

Key Takeaways from Using the Mortgage Calculator

A military mortgage calculator helps you see the full financial picture before you buy. By including your BAH, VA loan details, and local costs, you get a realistic idea of what fits your budget.

How to Prepare for Your First Military Home Purchase

Start by checking your VA loan eligibility and credit score. Then, use the calculator to test different scenarios, adjust loan terms, down payments, and interest rates until you find a comfortable range.

Homeownership is a big step, but with the right tools and preparation, you can make a confident, informed decision that supports both your financial stability and your family’s future.